Disclaimer: I’m not a certified tax consultant and you should always do your own research and consult a professional tax consultant.

This post describes the NHR specificalities for the IRS declaration in Portugal and how to declare them in the IRS web interface.

"Englobamento" (aggregation) vs autonomous tax rate

Income that carries a final withholding tax (when sourced in Portugal), or that is subject to an autonomous tax (when it comes from abroad, like capital gains from equities as we will see later), the taxpayer can opt to include it in the annual income tax return. This is called the "englobamento" option, and the final tax rate is then calculated as per Table 1. This option is advisable when the resulting tax rate is below the final withholding tax or autonomous tax.

IRS 2022 - Model 3

Annex H (Anexo H) - Deductible Household Expenses

It is mandatory to include Annex H (Anexo H) as part of the model 3 when the individual benefits from fiscal deductions (e.g. tax exemptions on qualified foreign income like dividend payments) or the deductions of some expenses (when the “englobamento” option is selected).

6. Deductible Household Expenses

Most deductible expenses are automatically communicated to the Autoridade Tributária e Aduaneira. As mentioned above, you can see them on this page of the Portal das Finanças. In case you want to override the reported expenses (because some are incorrect or because you want to add additional ones), the "Sim" option should be selected on field 01. For all other cases, the "Não" option should be selected, even if the Model 3 doesn’t include "englobamento" for any income category.

If the "Sim" option is selected, all the deductible expenses should be listed in the tables below, including those already reported to the AT.

Annex J (Anexo J) - Income obtained abroad

All income from the different categories (A,B, E, F, G and H) need to be reported in this section.

For instance, income from rent payments (category F) need to be added to section 7., while investment income (category E) like dividend payments need to be added to section 8.

The option "englobamento" option does not need to be selected if none of your income is subject to be taxed in Portugal because of an existing double tax treaty.

8. Investment income

In case you want to include a dividend income that does not need to be taxed in Portugal because of an existing double tax treaty, you need to select the option E11 Dividendos ou lucros - sem retenção em Portugal.

If the income has been sourced in Portugal or there is no existing double tax treaty the option E10 - Dividendos ou lucros - com retenção em Portugal needs to be selected. Portuguese banks by default charge you 28% for dividend payments and you need to inform them about your NHR status to avoid that. In case your bank already deducted the 28% withholding tax on your dividend income, of course, there is no need to report it in your annual IRS.

As mentioned above already, the "englobamento" option does not need to be selected if none of your dividends is subjected to taxes (E10).

9. Income from capital gains (category G)

Capital gains for share disposals from the previous year should be reported under section 9.2 Incrementos Patrimoniais de Opção de Englobamento > A Alienação Onerosa de Partes Sociais e Outros Valores Mobiliários.

The "código" should be "G01 - Alienaçao onerosa de açoes" for Stocks/ETFs/investment funds.

País da fonte = country where the investment is based (e.g. IE00B3XXRP09 is based in Ireland)

Since capital gains are subjected to taxes, you have the option to opt for the "englobamento" option in case you want to minimize the taxes paid (if you are in a lower tax bracket).

11. Declaration of foreign bank accounts (Contas de Depósitos ou de Títulos Abertas em Instituição Financeira não Residente)

Under this section you have to declare the IBAN and BIC codes of any foreign bank accounts you are an account holder or beneficial owner.

As per this official communication from the Autoridade Tributária, only accounts from credit institutions/banks have to be reported. There is an exemption for online banks like Transferwise or Monese as those do not operate as credit institutions .

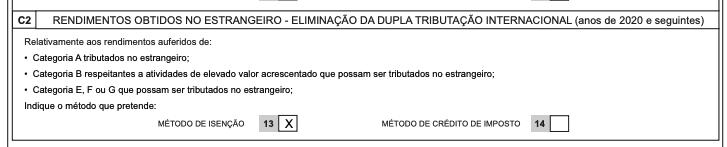

Annex L (Anexo L) - Non-Habitual Resident

Annex L is intended to declare the income earned by non-habitual residents in the national territory, in activities, previously listed, of high added value, whether scientific, artistic or technical (categories A and B), and is also intended to evidence the option of the method intended to eliminate international double taxation on that income, as well as on income from categories E, F, G and H obtained abroad.

6. Options for Taxation Regimes

Under section "C. Rendimentos Obtidos no Estrangeiro - Eliminação da Dupla Tributação Internacional" you should select the option "Método de isenção" in case you have any income from abroad (e.g. dividend payments) that should not be taxed in Portugal.