Taxes on Personal Income

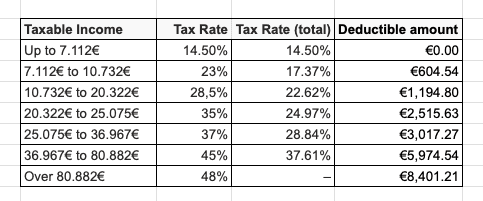

Residents in Portugal are taxed on their worldwide income at progressive rates varying from 14.5% to 48%. The progressive tax brackets are the following (source):

(Table 1)

An additional solidarity surcharge also applies (2.5 percent on the taxable income between EUR80,000 and EUR250,000 and 5 percent on the taxable income exceeding EUR250,000).

For each bracket there is a maximum deductible amount that lowers your taxable income. For instance, you can lower your taxable income by up to 502€ for rent payments. Each category and their corresponding limits can be found on your personal expenses page of the Portal das Finanças.

| Type of Expense | Possible Deductions |

|---|---|

| General Household Expenses | Deduction of general household expenses, corresponding to 35% of the amount of expenses incurred by any member of the household, limited to € 250 per taxpayer, whose taxpayer number is included in invoices for services or goods acquired in any sector of activity, provided these expenses are communicated to the Portuguese tax authorities, except for the sectors referred below. |

| Health expenses | Deduction of 15% of the following expenses: a) acquisition of goods and services which are exempt from VAT or liable to the reduced VAT rate of 6% (limited to €1.000); b) acquisition of other goods and services duly justified by a medical prescription; c) Health insurance premiums or contributions paid to mutualism associations or non-profit organizations that provide healthcare services. |

| Education expenses | 30% of all education expenses up to a limit of €800. |

| Housing interest or rent | 15% of debt interest, for contracts concluded until 31 December 2011, on loans made for acquisition of principal private residences in Portugal of a permanent house in the EU or the EEA, limited to €296. For the rental of a permanent house in the EU or the EEA the limit is €502. |

| Residential Care/Home | Deduction of 25% of the amount of residential care institutions. The limit is 403,75€. |

| Other expenses like: Car Repair, Restaurants, Monthly Pass Public Transportation, Veterinarian, Gym | 15% of the IVA payments can be deducted with a maximum deductible limit of 250€. |

Income categories

The income is divided into the following categories:

| Category | Type of Income |

|---|---|

| Category A | Employment income |

| Category B | Business and professional income |

| Category E | Investment income |

| Category F | Rental income |

| Category G | Capital gains |

| Category H | Pensions |

A detailed description of each income category can be found here.

Withholding Tax

Any income in the categories above, when sourced in Portugal, can carry a certain withholding tax. It can become final (called "retenção liberatória") when it matches the autonomous tax for that type of income, or it can be on account of the final tax payment, i.e. dependent on the final tax payment as per Table 1 above.

For example, interest payments from a Portuguese bank deposits (category E) have a withholding tax of 28% that is final, as it matches the autonomous tax for that income type. Being a NHR (non-habitual resident) might allow you to get a tax exemption on passive incomes (e.g. dividend payments) if the conditions are met.

On the other hand, employment income (category A) sourced in Portugal is a "payment on account" that is not final and depends on other factors like tax deductions and personal status (e.g. single vs married).